Real-time alerts

A window to refund or resolve a transaction before it converts into a formal chargeback and lands on your ratio.

Prevention, real-time dispute alerts and evidence-backed representment that keep your ratio under Visa's and Mastercard's 2026 thresholds, Visa flags “excessive” at 1.50% and 1,500+ combined items, in force since April 1, 2026. We build the evidence trail and the controls into the account from day one rather than reacting after a dispute lands.

Answer first

For a high-risk merchant, the chargeback ratio isn't a metric on a dashboard, it's the line between a working account and a terminated one. Cross the card-brand thresholds and you face per-item enforcement fees, mandatory remediation, intensified monitoring, and, if the ratio stays high, account termination plus placement on the MATCH list that makes getting boarded anywhere else genuinely hard. Mainstream processors handle this by freezing or dropping the account the moment disputes climb. We handle it by managing the ratio actively, all the way down, so it never reaches the cliff.

That means treating chargebacks as three connected problems: stopping disputes before they happen, resolving the ones that start before they harden into chargebacks, and winning back the ones that do with evidence. Each layer takes pressure off the next, and together they're what keep a high-risk account comfortably under the line even through a bad month.

The layers

A window to refund or resolve a transaction before it converts into a formal chargeback and lands on your ratio.

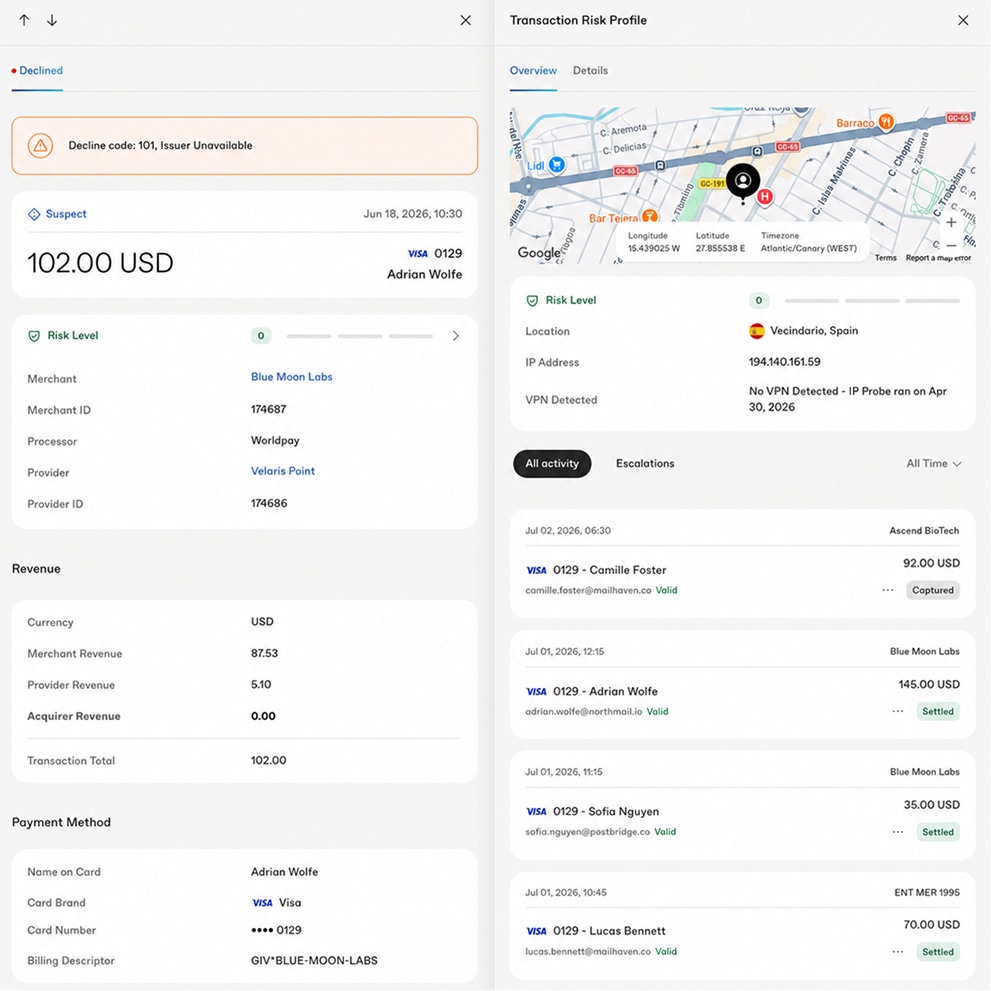

We contest the disputes that do land with the evidence that rebuts the claim, proof of delivery, accepted terms, transaction and AVS/CVV records, communication logs.

Recognizable billing descriptors, honest delivery and refund terms, fast customer service, and fraud screening that removes stolen-card disputes before they can start.

We track your combined fraud-and-dispute ratio against the current Visa VAMP and Mastercard lines, keeping you well clear rather than reacting at the edge.

Fraud vs. chargeback

Fraud prevention runs ahead of chargeback management: screening transactions for stolen-card and card-testing patterns before they post removes the disputes that would otherwise hit your ratio. The two layers work together, one stops the illegitimate transaction, the other defends the disputes that still come through.

How it works

You can't manage to a threshold you don't know, and the lines moved. Visa consolidated its monitoring into the Acquirer Monitoring Program (VAMP), and the merchant “excessive” threshold is a 1.50% ratio at 1,500 or more combined dispute-and-fraud items (TC40 + TC15) a month, live since April 1, 2026, with no warning tier and per-item enforcement. The ratio is combined fraud-and-dispute items measured against settled transactions, and Mastercard runs its own excessive-chargeback thresholds alongside it. Staying under 1% remains the safe operating guidance, because it leaves room to absorb a spike without crossing a line.

Most disputes are preventable, and prevention is the cheapest defense by a wide margin. For the disputes that do begin, real-time alerts give you a window to refund or resolve before they convert. What remains, we contest through representment, which only works when the records exist and are filed correctly inside the network's deadline. So we build that evidence trail into the account from the start: when a dispute lands, the case is assembled, not scrambled for.

FAQ

Under Visa's consolidated Acquirer Monitoring Program, a merchant is flagged “excessive” at a 1.50% ratio when also at or above 1,500 combined dispute-and-fraud items (TC40 + TC15) in a month, and the 1.50% line has been in force since April 1, 2026, with no warning tier. The ratio is calculated as combined fraud-and-dispute items against settled transactions. Staying comfortably under 1% remains the safe operating target, because crossing the threshold can carry per-item enforcement fees and, ultimately, account termination.

On two fronts. Prevent disputes before they happen, clear billing descriptors, honest delivery and refund terms, fast customer service, and fraud screening that stops stolen-card transactions before they post. And resolve the disputes that do start before they become chargebacks, using real-time alerts to refund or address a transaction inside the window. What's left, you fight with representment backed by evidence. Prevention plus alerts plus representment is what holds a ratio under the line, even through a spike.

Representment is the process of contesting a chargeback by submitting evidence that the transaction was legitimate, proof of delivery, the signed agreement or terms accepted, transaction and AVS/CVV records, communication logs. If the evidence rebuts the customer's claim, the funds can be returned to you. It only works when the records exist and are submitted correctly within the card network's deadline, which is why we build the evidence trail into the account from the start rather than scrambling after a dispute lands.

Crossing into excessive territory triggers escalating consequences: per-item enforcement fees, mandatory remediation programs, closer monitoring, and, if the ratio stays high, termination of the merchant account and placement on the MATCH list, which makes getting boarded elsewhere very hard. That's why threshold management isn't a back-office task; it's existential for a high-risk account. The whole point of active chargeback management is to keep you well clear of those lines.

Chargeback prevention is the cheapest layer by far, and most disputes are preventable. It comes down to removing the reasons a dispute starts: a clear, recognizable billing descriptor so customers don't dispute a charge they don't recognize, honest delivery and refund terms, fast customer service, easy subscription cancellation, and fraud screening that stops stolen-card transactions before they post. A large share of high-risk disputes are friendly fraud, a real customer disputing a real purchase, which clear descriptors and pre-dispute alerts head off directly. Prevention is what keeps the ratio low before representment ever has to defend it.

Win rates vary widely by vertical and by the quality of the evidence, so any single number is misleading, what's controllable is the evidence. Representment succeeds when the case rebuts the customer's specific claim with the right records (proof of delivery, accepted terms, AVS/CVV and transaction data, communication logs) filed correctly inside the network's deadline. The way to win more is to build that evidence trail into the account from the start, so when a dispute lands the case is assembled rather than scrambled for. Chargeback protection is a function of preparation, not luck.

Chargeback management isn't a separate purchase here, it's part of how every account is run, calibrated to your vertical's dispute profile at onboarding.