How Our Underwriting Works

AI risk screening scores your application in minutes, then a human underwriter reviews the full file and issues a written decision with your rate, reserve, and any conditions. You learn exactly why you were approved, not a black-box yes or no.

- AI screens, a human decides

- Same-day to 3 to 5 days

- US-based underwriting

The model

AI does the screening. A human signs the decision.

The industry treats underwriting as a black box on purpose. It's easier to decline you without explanation than to defend a decision. We built ours to be the opposite, and the structure is the reason it's both fast and transparent.

AI handles the first pass. It reads your application, pulls the risk signals from your category and processing history, and flags anything that needs a closer look in minutes, not days. Then a human underwriter takes the file, applies judgment the model can't, and writes the actual decision. The AI gives you speed; the human gives you a reason.

The process

The steps, start to boarding

Apply

Submit your business details, processing history, and supporting documents through the application.

AI risk screen

Our system scores your category, volume, ticket, model, and history against the risk band for your vertical and surfaces anything that needs human attention.

Human review

An underwriter reviews the full file and determines whether to approve, what rate within the published range applies, and whether a reserve is needed.

Written memo

You receive a decision in writing: your rate, your reserve and how it tapers, any conditions, and if declined, the reason and what would change it.

Board

Approved accounts are set up and go live.

The file

What we review

| What we look at | Why it matters |

|---|---|

| Monthly volume & average ticket | Sets your risk exposure and your pricing tier within the range |

| Card-present vs. card-not-present mix | CNP and recurring billing carry more dispute risk |

| Chargeback & refund history | The biggest single factor; benchmarked against VAMP/BRAM thresholds |

| Business model & legitimacy | Whether the model is boardable and correctly classified by MCC |

| Certifications | LegitScript for GLP-1/telehealth, age verification, and similar |

| Documentation | EIN, bank details, prior statements, category-specific paperwork |

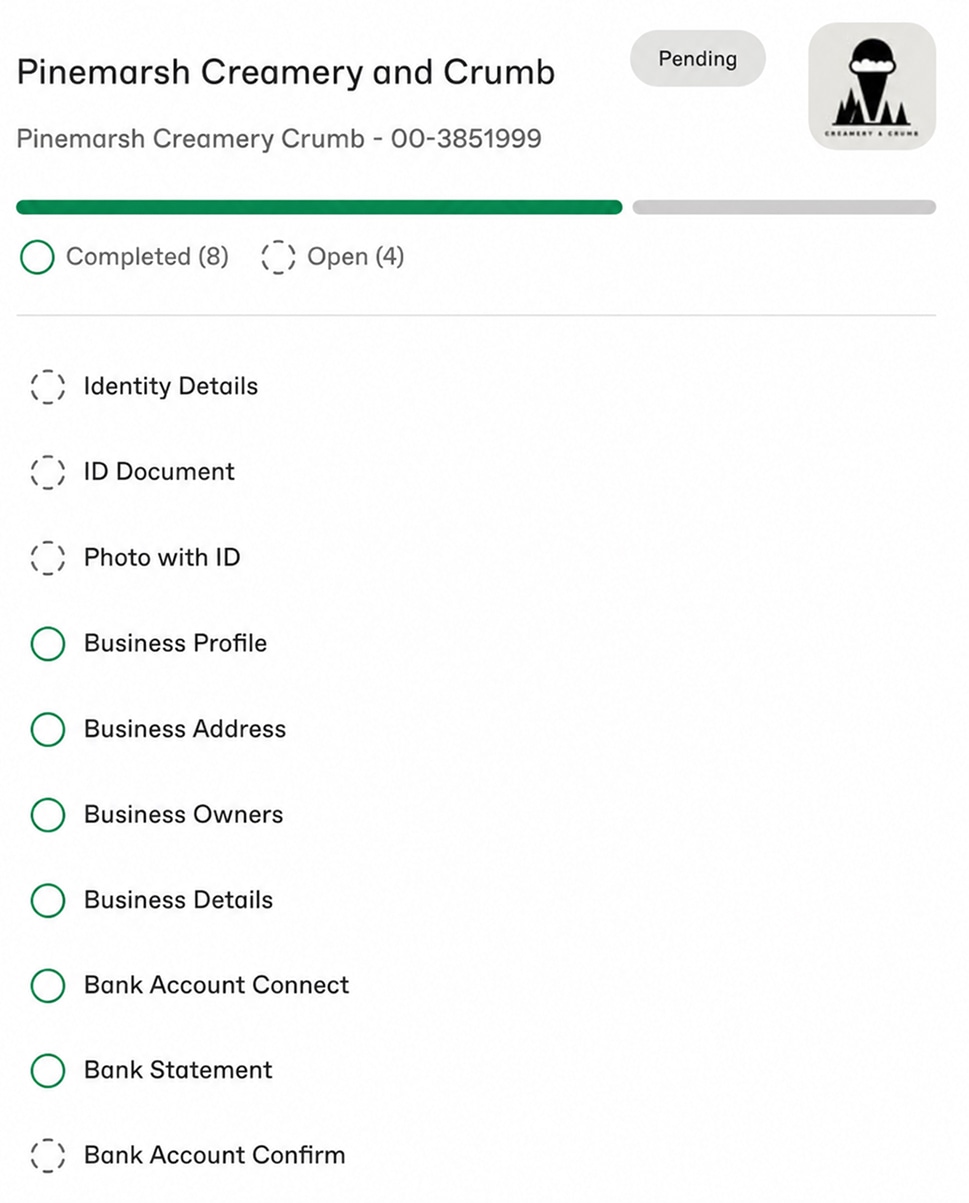

Identity & KYB

Identity verification and KYB during onboarding

Part of underwriting is simply confirming you are who you say you are, and that the business is real and legitimately yours to operate. That's the KYC/KYB layer, Know Your Customer and Know Your Business, and it runs as part of onboarding rather than as a separate hoop. We verify the business entity and its EIN, the beneficial owners and their identities, the bank account that funds will settle to, and that the stated business model matches what you actually do. It's the same identity and business-verification work a sponsor bank requires before any merchant can be boarded.

For most legitimate merchants this is quick and invisible, the documents you already have (EIN, bank details, ID, prior statements) are what's needed, and the AI screen flags only genuine mismatches for a human to look at. KYB matters because a clean, verifiable business is easier and faster to board: the gaps that slow approval are usually missing or inconsistent verification documents, not the underwriting decision itself. Getting your identity and business records in order before you apply is the single best way to speed up the path to a live account.

Gated categories

When a category needs sponsor concurrence

Some verticals can't be boarded on a standard path. Pure card-not-present nutraceuticals, marketplaces and PayFac models, commercial crowdfunding, and MLM/direct sales require sponsor concurrence, meaning our sponsor bank pre-approves the merchant before boarding.

That adds two things: extra documentation (more detail on your model, compliance, and flow of funds) and extra time. It is not a soft no; plenty of these merchants get approved. We'd rather tell you the realistic timeline at the start than let you assume a three-day turnaround on a three-week path.

The memo

A written rationale, not a black-box no

When a mainstream aggregator offboards a merchant, the message is a template and the reason is risk. That helps no one. Our written memo tells you the actual decision logic: the rate and why, the reserve and when it tapers, the conditions, and on a decline, the specific issue and whether it's fixable.

If your vertical carries a rolling reserve, the memo states the percentage, the hold period, and the conditions under which it steps down as your account builds a clean history. That transparency is also a discipline on us: a decision you have to explain in writing is a decision you have to be able to defend.

A written decision

Every file, tracked to a decision

Underwriting here is not a black box. Every file moves through a tracked checklist, AI screening, then human review and KYB, and you get a written decision with your rate, reserve, and any conditions. No automated yes that turns into a freeze three months later.

- Tracked from application to boarding

- A human reviews the file and signs the decision

- Rate, reserve and conditions in writing

FAQ

Underwriting FAQ

How does high-risk merchant underwriting work?

Underwriting is the process of assessing whether, and on what terms, a business can be boarded for card processing. At GivePayments it has two layers: AI risk screening evaluates your application data, processing history, and category signals in minutes, then a human underwriter reviews the file and issues a written decision with your rate, reserve, and any conditions. Compliant, well-documented applications are typically boarded same-day to 3 to 5 business days.

Why was my merchant account declined?

Most declines trace to one of a few things: a chargeback history above the card-brand thresholds, a business model in a prohibited category, missing certifications (such as LegitScript for GLP-1 or telehealth), incomplete or inconsistent documentation, or a mismatch between your stated MCC and what you actually sell. The advantage of a written decision is that you learn which one, and usually what would change the answer, instead of getting a black-box no.

How long does high-risk approval take?

For mainstream high-risk verticals with clean documentation, typically same-day to 3 to 5 business days. Categories that require sponsor concurrence (pure card-not-present nutraceuticals, marketplaces, PayFac models, commercial crowdfunding, MLM) take longer because they involve an extra layer of pre-approval and additional documents. We tell you which path you're on before you start.

What do underwriters look at?

Your monthly volume and average ticket, card-present versus card-not-present mix, recurring-billing model, chargeback and refund history, the legitimacy and compliance of your business model, required certifications, and your supporting documents (EIN, bank details, prior processing statements, and category-specific paperwork). Together these set your risk band, your rate within the published range, and whether a reserve applies.

Keep exploring

Ready to start?

Apply and get a written decision with your rate, reserve, and any conditions. You learn exactly why, not a black-box yes or no.